The second quarter and the weeks that have followed have been a swift reminder of the effects of monetary policy. The Fed has been applying the levers available to them, and worldly events have whipsawed our attention in a better-than-TV news cycle. There is so much to comment on, but of particular attention is a renewed interest into the foundational blocks of our economy that are shifting in ways that appear as ripples, but may be tectonic in nature.

At Construct, we believe the window for long term opportunity to reimagine these spaces is more imperative than ever. Below are the levers and signals we are watching most closely that reaffirm the importance of transforming the core industries that drive productivity into tech-driven industries.

Economic policies enacted over the past two years, culminating with now-rising interest rates and other measures to curb inflation, have shone light onto how some of the past remedies propped up but did not set up the economy for a sustained recovery or future growth. Our production systems, supply chain, and transportation networks have been underinvested in for decades and neglected by technologists. The compounding technical debt from manual processes and outdated systems (including but not limited to fax machines, which are still in use!) created an increasing burden. And yet, these industries that drive the goods and services we consume daily are too big to fail — they have consistently made up over 50% of the GDP for decades, both in boom times and challenging economic climates. The challenge to transformation is that these industries are architected in ways that cause cascading failures when one step in the supply chain goes awry. As a result, corporate leaders view changes as high risk. However, the whipsaw of the economy over the past two years has made change imperative — these industries are simply not set up to sustain economic demands anymore.

Here are three examples of recent economic swings and a window of clear demand for long-term technological transformation of each:

- Elevated inflation, especially around gas prices, has shifted consumer demand. Electric vehicles have reached a tipping point, creating opportunities surrounding EV adoption.

- The shift in inventory management from just-in-time to stockpiling has drastically increased inventory levels. This has raised the bar on the level of visibility required within the supply chain, and the solutions required to enable this.

- There has been consistently low unemployment levels coupled with a long-term, projected contraction in the labor pool. Automation is now a necessity to improve productivity.

Let us discuss each of these…

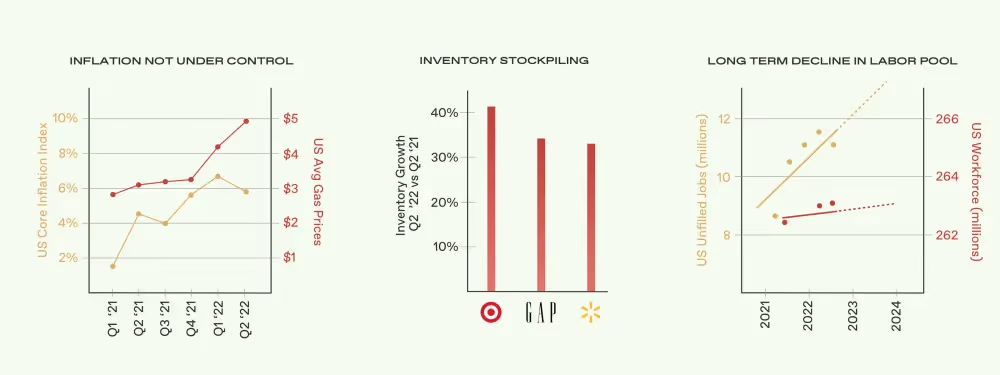

While inflation got out of control, rising gas prices, in particular, have had the most recent and direct effect on consumer spending, impacting trucking costs and pushing consumers towards electric options. In Q1 2022 we saw electric new car sales reach 5% of total car sales, surpassing the “technology tipping point” from early adopters to mass adoption. Since then, as gas prices have soared, electric new car sales increased by 24%, and it is now expected that electric sales in the US will hit 25% of new vehicle sales before 2025, 1-2 years ahead of expectations. With the growth in electric car sales, the need to focus on infrastructure is imperative, and ChargeLab is positioned to scale, right as the broader industry needs their solution of EV charging software.

Major retailers, from Walmart to Target to Gap, are saddled with record levels of inventory — inventory levels are 30%–45% higher than they were a year ago. Simultaneously, shipping ports and container ships are clearing their log jams, delivering more long overdue inventory and exacerbating the problem. As a result, freight rates are declining precipitously. The spot market for freight fulfillment has all but disappeared and linehaul rates have dropped 20%–25%. Going forward, retailers are looking to quickly terminate relationships with the most unreliable suppliers, and are becoming increasingly picky about the brands and suppliers they work with. Providers with superior communication, visibility, and transparency will be rewarded with continued business. Buffalo Market — a new and rapidly growing, true tech-enabled food distributor — provides large retailers such as Costco and Walmart reliable and more cost-effective delivery of some of the best mid-tail and good-for-you brands with transparency into pricing and reliability of delivery.

The jobs report published on Friday cited that unemployment is still at record lows at 3.5%. It’s hard to assess the importance of this barometer given that there is a dislocation in how and where professional jobs function best (remote work and job switching is at a peak). On top of this, there is a protracted decline in available workers and thus, employment may not be as clear a measure of our economy’s health as it has been historically. Regardless of incentives for workers to pursue new jobs, there could be an ongoing lack of labor supply to support our GDP. The labor pool is set to grow just 0.2% a year from 2024 to 2031 — baby boomers are retiring, millennials are reaching middle age and younger generations are significantly smaller than their predecessors. The decline is magnified by a growing skills gap — trade schools have been on the decline for decades and 77% of manufacturers say they will have ongoing difficulties in attracting and retaining workers this year and beyond. The diminished labor pool presents a need to find alternative sources of productivity, such as automation, which continues to drop in cost. For example, robotics cost 1/4 of what they did just 5-6 years ago. Deeper automation offers the long-term solution to labor shortages. Chef Robotics works with food manufacturers whose workers have been actively complaining about unsatisfactory treatment and cold conditions in the plant. Automation of these processes provides a clear answer.

Over the past three months, we have redoubled our primary research to form our conclusions directly from industries where we focus. We’ve actively sought out and interviewed potential buyers of new technology in these sectors to understand the impacts of these macro economic factors. So far, we have heard renewed interest in automation solutions and a strong imperative for complete visibility into the supply chain. The pandemic introduced unprecedented demand and growth; it was a time of “drinking from a firehose” — for founders, investors, corporates alike — with the wild swings in both supply and demand. It was not feasible for the industrial sector to change their processes overnight. But the potential cost savings, productivity gains, and efficiencies can no longer be ignored. And, that long overdue time for investment is now.